How to be a responsible credit card holder and why it matters

A credit score can be a helpful tool for your overall financial wellness. Unfortunately, rules and regulations surrounding credit scores can be complex and unclear. Read on to learn the importance of a good credit score, its components, and how to use a credit score to impact your financial health.

WHAT IS THE PURPOSE OF A CREDIT SCORE?

Put simply, a credit score is your financial report card. It allows lenders to assess your trustworthiness as a borrower. A good credit score not only grants you easier access to lower interest rates on loans, but it can also help you rent an apartment, finance a car, or pay down a mortgage. In short, your credit score helps you navigate the lending side of the financial world, and even gain greater financial success.

WHAT ARE THE COMPONENTS THAT MAKE UP A CREDIT SCORE?

Your payment history: Do you have a record of paying your bills, in full and on time? Doing so will boost your credit score. Paying bills on an inconsistent basis (or ignoring them completely) will lower your score. FYI, paying the minimum monthly payment is not paying your bills in full. Paying only the monthly minimum will negatively impact your credit score. Don’t be tricked by that sneaky number. Live within your means and pay your bills on time. Pro tip: Utilize due dates in your calendar, or use the reminders app on your phone, to remind you to pay your bills.

The amount you owe: Do you approach or reach your credit limit each month? The ratio of the amount you spend and the limit on your credit card is called credit utilization. It is best to keep this ratio high (i.e. 1:10 not 1:1). Leaving room between the amount you spend in any given month and the limit on your credit card will boost your credit score, while closely approaching your credit limit each month (or reaching it) will lower your credit score.

The length of your credit history: How long have you had a credit score? The longer the better! If you do not currently have a credit card, make sure you are responsible enough to own one before rushing to get one. Remember, it is better to be a responsible borrower for a shorter period of time than an irresponsible borrower for a longer period of time.

Your credit mix and new accounts: How many accounts do you have? Utilizing a variety of different borrowing options (i.e. a combination of a mortgage, an auto loan, and student loans) isn’t bad if necessary. In fact, it can actually be helpful! Try to keep open accounts to a minimum, even if you only use some accounts sparingly. Opening multiple accounts can cause lenders to be more suspicious, which in turn can lower your score. So, yes, you heard me. You might need to cancel that Hawaiian Airlines card, even if you save $150 every 2 years for your biannual Hawaii trip.

Aside from these factors, lenders may also look at your salary, occupation and job title, and employment history. These additional factors will not actually change your credit score, but they can be used in addition to your credit score to assess your trustworthiness.

WHAT IS A GOOD CREDIT SCORE?

By assessing each of these components, a three digit credit score is generated, ranging from 300-850. Any score over 700 is considered a good score.

SO, WHAT DOES IT LOOK LIKE TO BE A RESPONSIBLE CREDIT CARD HOLDER?

Sure, this information can be helpful, but how can it be applied to everyday life? Let’s look at an example.

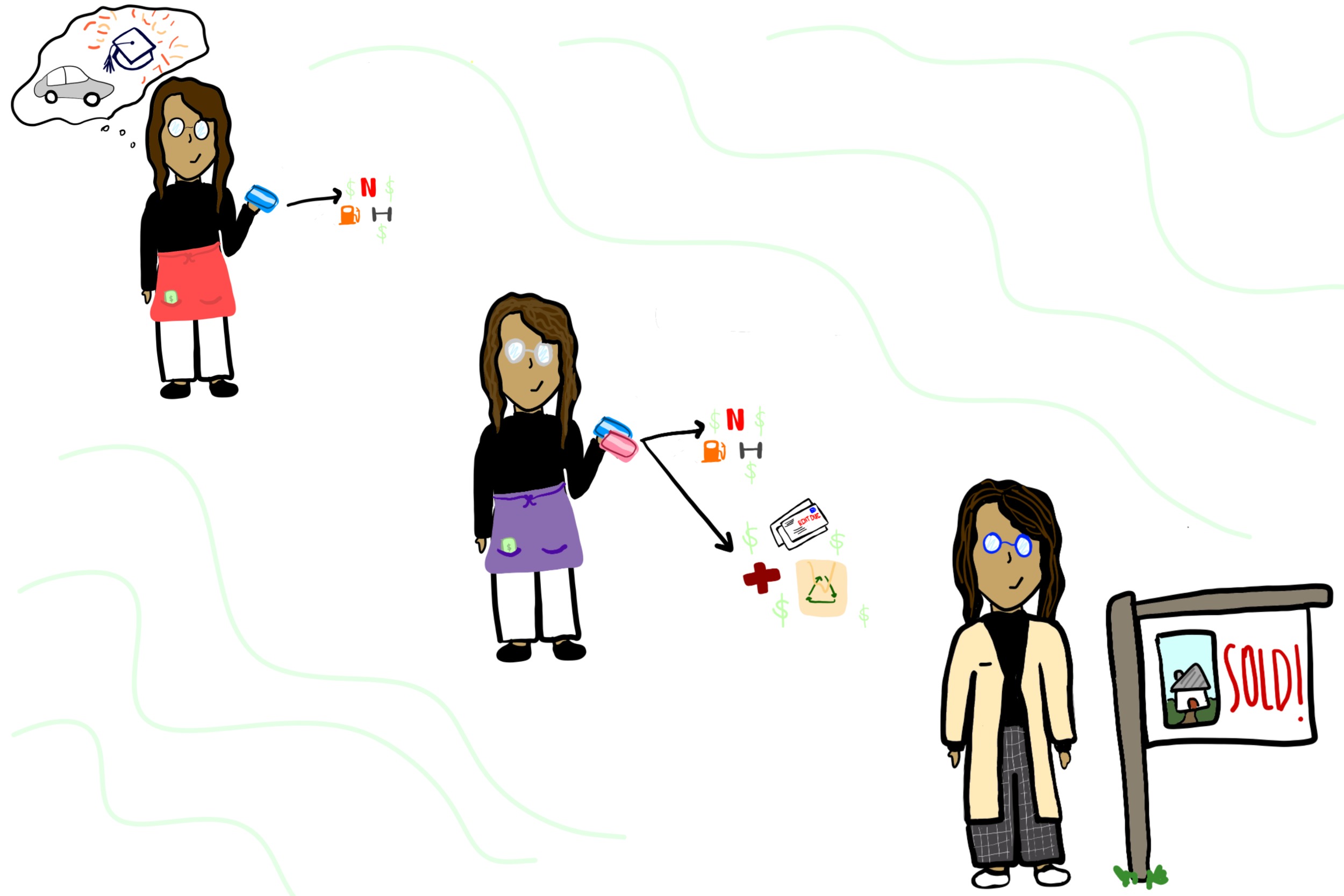

SOPHIA IS A RECENT COLLEGE GRADUATE.

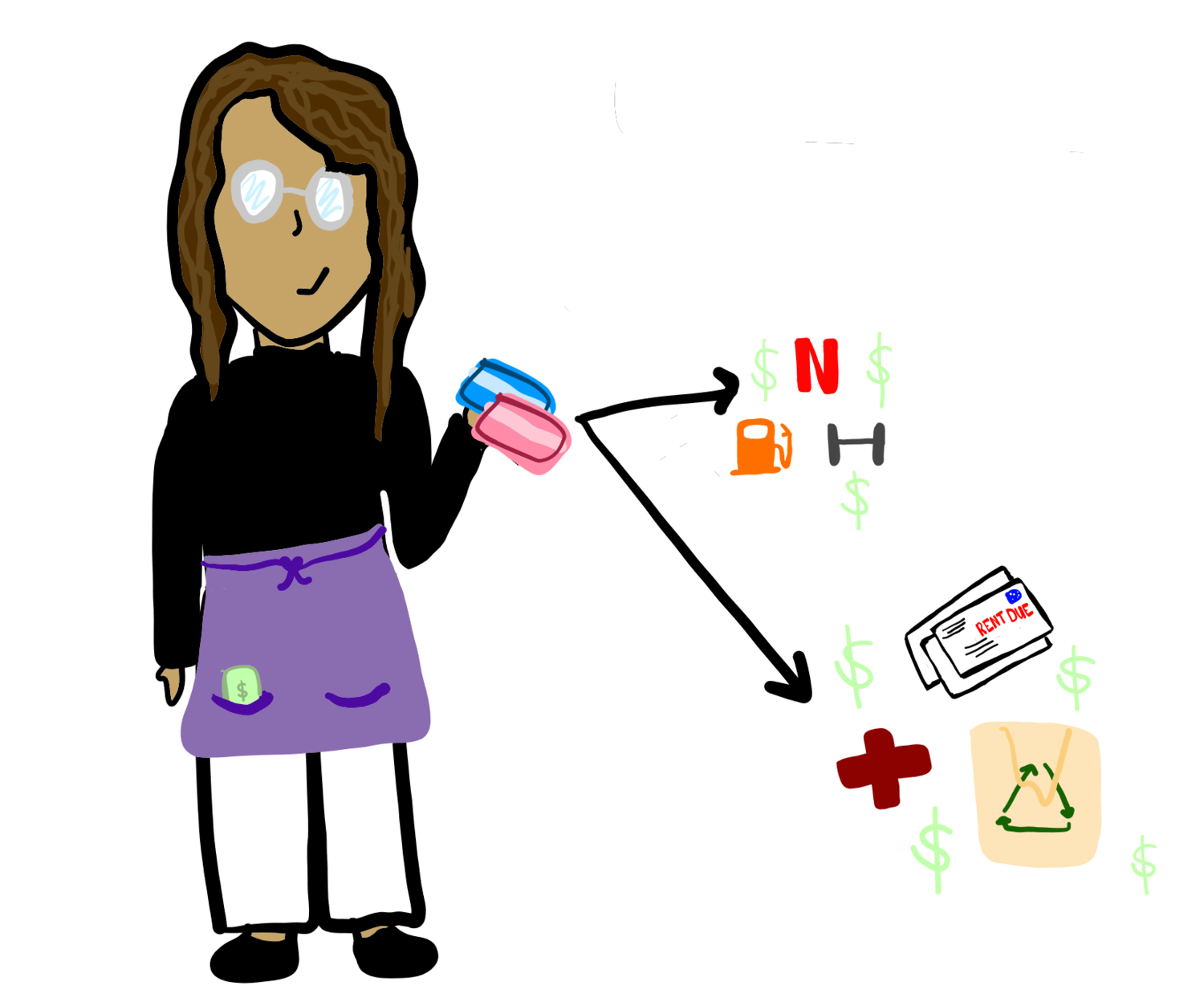

She just received her first full-time job and is looking to build her credit score. She applies for a credit card that has a low credit limit and only uses it for her regular monthly payments: gas, Netflix, and her gym membership. She lives within her means, knowing she has other payments to consider, such as her student loans and auto loan.

SOPHIA GETS USED TO LIVING OFF OF A BUDGET.

Every month, Sophia remembers to pay her credit card bill, and pay it in full. As a young lender, it is important for her to stay on top of her monthly payments.

AS SOPHIA AGES, SHE SOLIDIFIES HER GOOD SPENDING HABITS.

She opens another credit card account that has a larger spending limit, and uses it conveniently for groceries, bills, and other expenses—still living within her means and paying her bills on time.

ALL HER DAILY MONEY HABITS PAY OFF.

Her credit score has deemed her a trust-worthy lender, and she is able to lock-in favorable rates for the mortgage of her first home!

Related Articles